Being self-employed comes with lots of perks. As your own boss, you don’t have to answer to anyone else, and you have complete control over your clients and your work-life balance.

But as you’ll quickly learn, working for yourself also has its fair share of headaches—including taxes.

Paying taxes as a self-employed individual isn’t quite as simple as being a W-2 employee with a steady paycheck. To avoid penalties from the IRS, you need to understand self-employment taxes and how they work.

As someone with first-hand experience calculating and paying self-employment taxes, I’ve put together this complete guide for freelancers, entrepreneurs, and anyone else who is self-employed.

What is Self-Employment Tax?

Self-employment tax refers to Social Security and Medicare taxes for people who work for themselves.

Just like other workers who have Social Security and Medicare taxes withheld from their paychecks, self-employed individuals must pay these taxes as well. Traditional employees pay a little less than 8% of their gross income towards Social Security and Medicare, and the employer matches that contribution. But self-employed individuals are responsible for paying the total 15.3% tax on their own.

It’s important to know that self-employment taxes only refers to Social Security and Medicare. There are other income taxes you’ll be paying to the federal government and state that don’t fall into this category.

The Basics of Self-Employment Tax

Self-employment taxes can be a bit confusing, especially if you’re a beginner. But we’ll break down the core components of these taxes below so you’ll have clarity on how it works.

Self-Employment Qualifications

First, you need to figure out whether or not you qualify for the self-employment tax. Generally speaking, anyone in the following categories is considered self-employed by the IRS:

- Sole proprietors or independent contractors that have a trade or run a business

- Members of partnerships that carry a trade or a business

- Anyone in business for themselves, including part-time businesses

That third bullet point is pretty clear-cut. If you work for yourself, you’re considered self-employed—even if it’s just part-time or a small side hustle.

Assuming you qualify as self-employed, now you need to determine whether or not you’re subject to the self-employment tax. Any self-employed individual with annual net earnings of $400 or more must pay self-employment taxes. Church employees with an income of $108.28 or more are also subject to self-employment taxes.

In short, if your self-employed business or trade had a net profit of at least $400, you owe self-employment taxes.

It’s also worth noting that these tax rules apply to everyone who is self-employed, regardless of age. So even if you’re already receiving Social Security or Medicare, you still owe self-employment taxes based on the qualifications listed above.

Self-Employment Tax Rate

The tax rate for self-employment taxes is 15.3%. This number comes from two parts—12.4% for Social Security and 2.9% for Medicare.

Generally speaking, 92.35% of your net earnings from self-employment ventures are subject to self-employment taxes.

The amount of taxes you need to pay on the Social Security portion of the self-employment tax is capped based on your earnings, and the threshold changes each year. In 2020, the first $137,700 of your wages, tips, and net earnings from self-employment was subject to the 12.4% tax rate for Social Security self-employment tax. In 2021, that threshold is $142,800.

There is no cap for the 2.9% Medicare portion of self-employment taxes. In fact, individuals with net earnings above $200,000 must pay an additional 0.8% for the Medicare portion, bringing the total Medicare tax rate to 3.8%.

Self-Employment Tax Deductions

Unlike the rest of your income taxes, the self-employment tax is assessed on your net earnings—not your adjusted gross income (AGI).

For example, let’s say you’re taking the standard deduction on your individual tax return, which was $12,400 in 2020. That deduction doesn’t apply when you’re calculating self-employment taxes.

If your net earnings from self-employment are $100,000 for the year, you’ll be paying self-employment taxes based on the full $100,000. Even if the taxable income on your individual return is $70,000 based on other deductions, it doesn’t affect the self-employment tax rate.

However, self-employed individuals can deduct the employer-equivalent portion of the self-employment tax when calculating their AGI—ultimately lowering their taxable income for the rest of the income taxes owed.

Section 2042 of the Small Business Jobs Act allows some self-employed individuals to deduct the cost of health insurance premiums. This deduction is taken into consideration when calculating net earnings from self-employment.

Certain factors impact this deduction. For example, you can’t take the deduction if you’re eligible for an employer-sponsored plan. You also can’t take the health insurance deduction if your self-employed business took a net loss on the year.

Estimated Quarterly Payments

Many self-employed individuals are subject to quarterly tax estimates. According to the IRS, you need to make quarterly tax payments if you expect to owe $1,000 or more in taxes when your return is filed.

Quarterly payments are due to the IRS by the following dates:

- April 15

- June 15

- September 15

- January 15

Depending on your location, you might also owe estimated quarterly payments to your state’s tax office.

Your estimated payments are based on a combination of your self-employment tax and income taxes. In short, your self-employment tax for Social Security and Medicare must be taken into consideration when you’re making these payments.

While these might just be estimates, it’s important to make sure they’re somewhat accurate to avoid under-withholding. If you don’t pay enough in quarterly estimates, you might be subject to additional penalties imposed by the IRS.

Generally speaking, you can avoid these penalties by paying at least 100% of the taxes shown on your return for the previous year or at least 90% of the taxes owed for the current year.

3 Tools to Help With Self-Employment Taxes

There are many great tools, software, and technology on the market that can help you navigate the waters of self-employment taxes. The following solutions are my favorite options for beginners:

#1 — Wave Accounting

Wave has a wide range of financial apps built for entrepreneurs. With Wave Accounting, it’s easy to gain control over your finances and prepare for tax season. The accounting solution is 100% free, so there’s no risk involved with getting started. Compared to some of the other accounting solutions on the market, Wave is arguably the easiest to use for self-employed entrepreneurs.

I like Wave’s ability to help you manage your cash flow and expenses. It can connect with an unlimited number of bank accounts and credit cards and automatically put those transactions into your bookkeeping records. When it comes time to pay your taxes, Wave organizes everything based on income, expenses, payments, invoices, and more—so it’s super easy to figure out how much you owe.

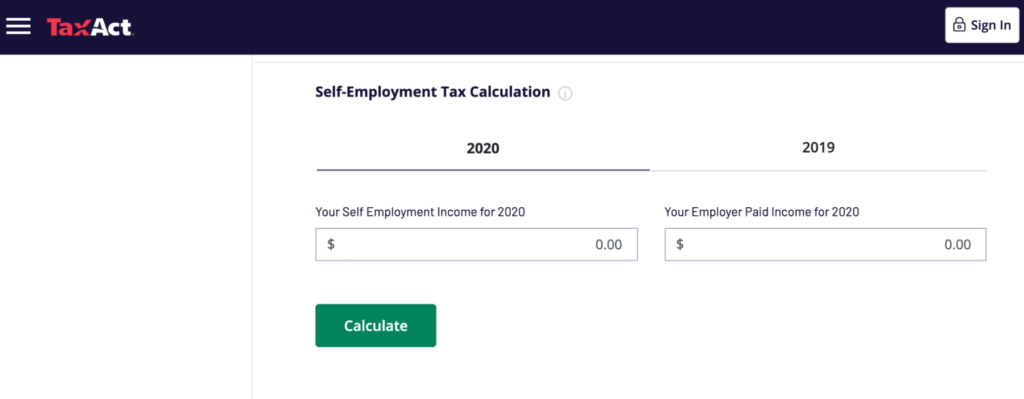

#2 — TaxAct

TaxAct is a popular solution in the tax preparation software category. But unlike some of the competitors in this software niche, TaxAct has excellent tools designed for self-employed individuals, including a free self-employment tax calculator. Beyond this free tool, TaxAct has a Self-Employed plan that starts at $94.95—which is really affordable considering the perks you get.

It’s a great option for those of you who want a self-service solution to paying taxes but without the hassle of doing everything on your own. TaxAct has a maximum refund guarantee and gives you seven years of access to your returns. Another advantage of TaxAct is its Xpert Help solution—connecting you one-on-one with CPAs and tax experts whenever you have questions. The Self Employed plan plus Xpert Help bundled together starts at $179.95.

#3 — QuickBooks

QuickBooks is an industry leader and arguably the most well-recognized name in the accounting software space. They have solutions for businesses of all shapes and sizes, including self-employed individuals. The software makes it easy to automatically track business transactions by syncing with your bank accounts and credit cards.

You’ll also be able to store receipts by taking pictures with the QuickBooks app, and the software will automatically match them to your business expenses. One of my favorite features is the quarterly tax estimation tool—helping you avoid surprises and late fees so you know exactly what you owe. Plans for self-employed individuals start at just $7.50 per month.

3 Tricks For Self-Employment Tax

Nobody likes paying taxes. But these few quick tips and best practices can make your life much easier and help save you some money.

Trick #1: Save at Least 25% of Earnings For Quarterly Taxes

One of the biggest challenges for self-employed individuals is managing tax obligations. Since your taxes aren’t automatically deducted from a paycheck, it’s tough to figure out how much you’re actually making after taxes as you get paid throughout the year.

Your final tax numbers, including self-employment taxes, will vary based on a wide range of factors. These include your net income, AGI, deductions, expenses, credits, filing status, and so much more.

But here’s a simple trick I’ve used for years, and it works for the vast majority of self-employed individuals: Take at least 25% of your earnings and put them aside for taxes.

Let’s say you’re a 1099 contractor that nets $4,000 in January. Put $1,000 into a separate account, and draw from those funds when it’s time to pay your Q1 estimates by April 15.

Putting this money into another account immediately will help you avoid unpleasant situations where you don’t have enough cash to pay your estimates.

You can do it at the end of each month after calculating your earnings, or you could take 25% every time you get paid by a client and put that money in a separate account. It will work out either way, so it just depends on which system works best for you.

Trick #2: Hire an Accountant

I can’t stress this enough. Hiring an accountant will save you tons of time and money.

Most self-employed individuals aren’t accounting experts. Trying to become one in order to save a few hundred dollars isn’t worth it. In most cases, an accountant can give you tax advice that’s easily worth the cost of their services.

For example, they might suggest opening a SEP IRA—a retirement account for self-employed individuals. Contributions to your SEP can help lower your taxable income.

Your accountant will also make sure all of the calculations are done correctly. The IRS has so many rules and stipulations for different scenarios that it’s nearly impossible to accurately calculate self-employment taxes and income taxes on your own.

Can it be done? Absolutely. But personally, the extra $500 or so to have an accountant file your returns is well worth the countless hours of headaches and aggravation.

Trick #3: Carefully Track Your Business Expenses

Lots of self-employed individuals poorly track expenses. This is something I was guilty of for years when I first started working for myself.

But expense tracking can really help you save money on your self-employment taxes and income taxes alike.

Unlike tax deductions, business expenses directly impact your net income. Lowering your net income reduces the amount you have to pay in self-employment taxes.

For example, your new desk, office chair, and printer for your home office could all be expensed.

Using software and tools, like some of the options listed earlier in this guide, can make it easier to track expenses. Trying to manually keep track of paper receipts can quickly turn into a disaster.

What to Do Next

Now that you have a firm grasp on self-employment taxes, it’s time to take your business to the next level.

I strongly recommend that you take advantage of modern technology to get your finances in order. Check out our guide on the best accounting software for small businesses. This is much more efficient than managing your finances on a spreadsheet.

As previously mentioned, having different bank accounts makes it easier to prepare for taxes and pay quarterly estimates. Our guide on the best business checking accounts can help you get organized here.